TL:DR version - No

Never been systematically explored? We have these maps in Vizsla's own PRs and presentations:

How much are the mines producing? How big is the mill? Surely Vizsla will have some historic production figures to support the $23M purchase price?

How much are the mines producing? How big is the mill? Surely Vizsla will have some historic production figures to support the $23M purchase price?

What really interests me is that Vizsla keep telling us this:

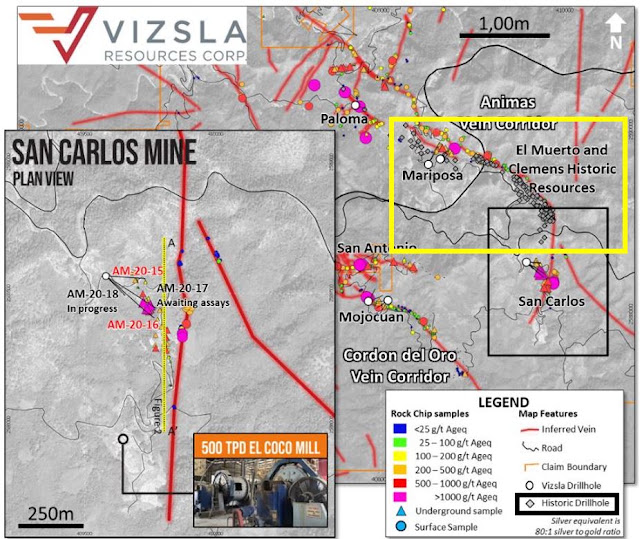

We have 2 areas with historic resources and a long section of the Animas vein with >100 holes on it. Maybe the drilling was done by the mine operator? Fortunately, Vizsla give us a helping hand and tell us at the bottom of the Panuco project page (just before the photos).

So, I went over to Sedar and downloaded the report. A full 100 pages of geological fun, which gently summarized the historic, non-systemaic work done by Silverstone, who only managed to drill:

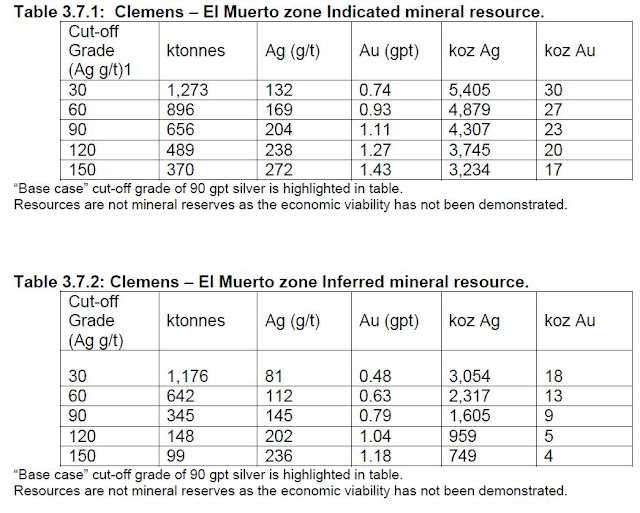

Thta's only 21,641m in 200 holes. I'm guessing that Vizsla forgot about these holes. My guess is that the core doesn't exist anymore, or that looking at the long section above a chunk of the Clemes/Muerto zone was mined, and if we have a look at them, we see:

That they are a bit shite! Silverstone only managed to drill >21km of drilling in 2 holes and defined a small, low grade resource. Why?

We have 2 options:

- Silverstone were crap, and managed to drill all the shite areas again and again

- The mineralization at Copala is hosted in very small high-grade ore-shoots

Let us not question the competence of Silverstone, and focus on the second point - small, inconsistent zone of mineralization. We can look for this in a number of ways:

Directly

- High-grade mineralization restricted to 1 or 2 holes surrounded by lots of nothing

- high-grade intervals not joining up - the vein's the same, but suddenly the silver and gold have gone on holiday to a narrow foot-wall or hanging-wall vein

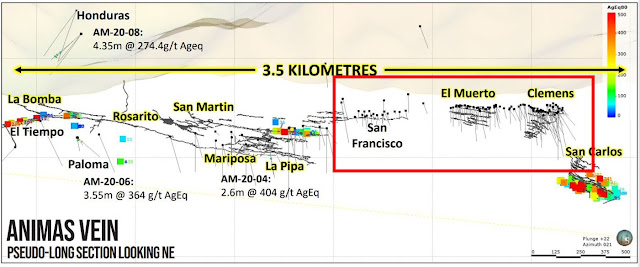

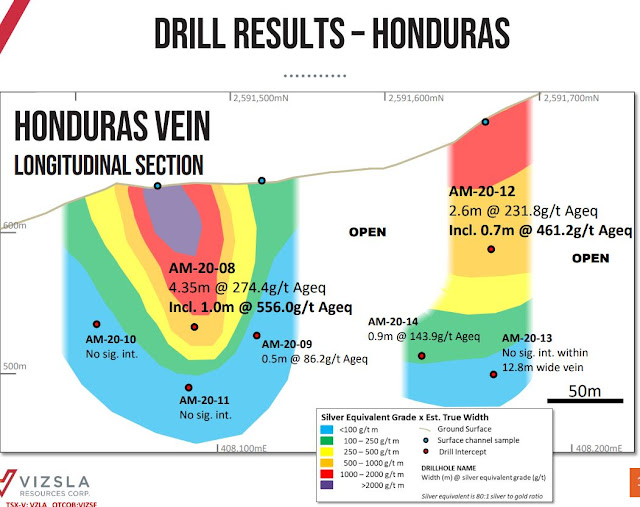

Here is a long section from the Honduras vein at Copala

Look at the scale - holes AM-20-08 is only 50m from holes 09, 10, and 11. We go from good to nothing in 50m.

We see the same at the Napoleon discovery

There are some good drill-holes here, and the drilling here is at its early stage, but we can see that the high-grade intercepts are jumping from structure. We can also see that the "F" and "G" veins don;t appear to be very continuous, as they aren't intersected by hole NP-20-07 just 20m away.

Indirectly

- "Missing" intervals - we see on a map or section "waiting assay results", but the results never arrive

- "Missing holes" - were have the results for holes 01, 02, 05, 09 - WFT happened to holes 03, 04 and 06 --> they hot feck all is what happened.

Missing holes can also be expanded into an entire drill program going AWOL - this means all the holes were crap, and the company doesn't want to hurt everyone's feelings.

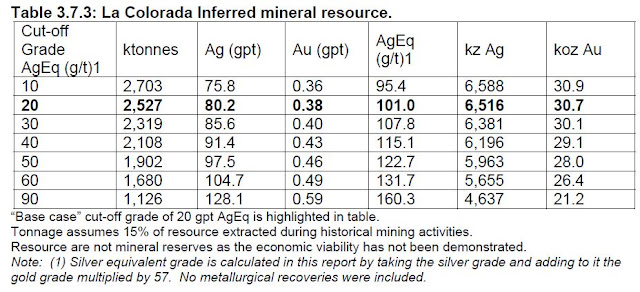

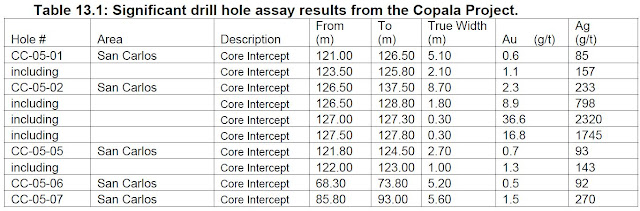

So, going through the technical report (you can download it from here), there is a table of all the narrow, high-grade hits (table 13.1)

This is just the first few intervals, there are 3 more pages for you to look at, but they look very similar to what Vizsla are getting and this is what they got:

This is crap for an underground mine, 370Kt @ 370 g/t AgEq, you can't do much with that.I hope Vizsla do find some massive ore-bodies, but the data presented by Silverstone and what we're seeing in the initial 2020 drilling data is that the high-grade mineralization is found is discrete, small ore-shoots.

One final comment, we're told this on the website:

BTW - Vizsla - Fresnillo don't own the Zacatecas district. Pan American and Capstone have a good chunk and ~50% was just sold by Santacruz silver to Zacatecas Silver earlier this year. You may want to correct that.